Tax-Advantaged Investments for Accredited Investors

Proactive tax-management approaches designed to help accredited investors address capital gains exposure, concentrated positions, and planned liquidity events.

Do I Qualify?Choose Your Perspective

This page adapts to show you what matters most. Select your role below.

1031 Exchange to DST Guide

Everything you need to know about transitioning from investment property to passive, tax-deferred income through Delaware Statutory Trusts.

You've built wealth through real estate. Now it's time to protect it.

The BasicsWhat Is a 1031 Exchange?

A 1031 exchange — named after Section 1031 of the Internal Revenue Code — allows investors to defer capital gains taxes when selling investment or business property by reinvesting the proceeds into "like-kind" replacement property. This powerful strategy has been a cornerstone of real estate investing for decades.

Why Consider Delaware Statutory Trusts?

DSTs have become an increasingly popular replacement property option within 1031 exchanges.

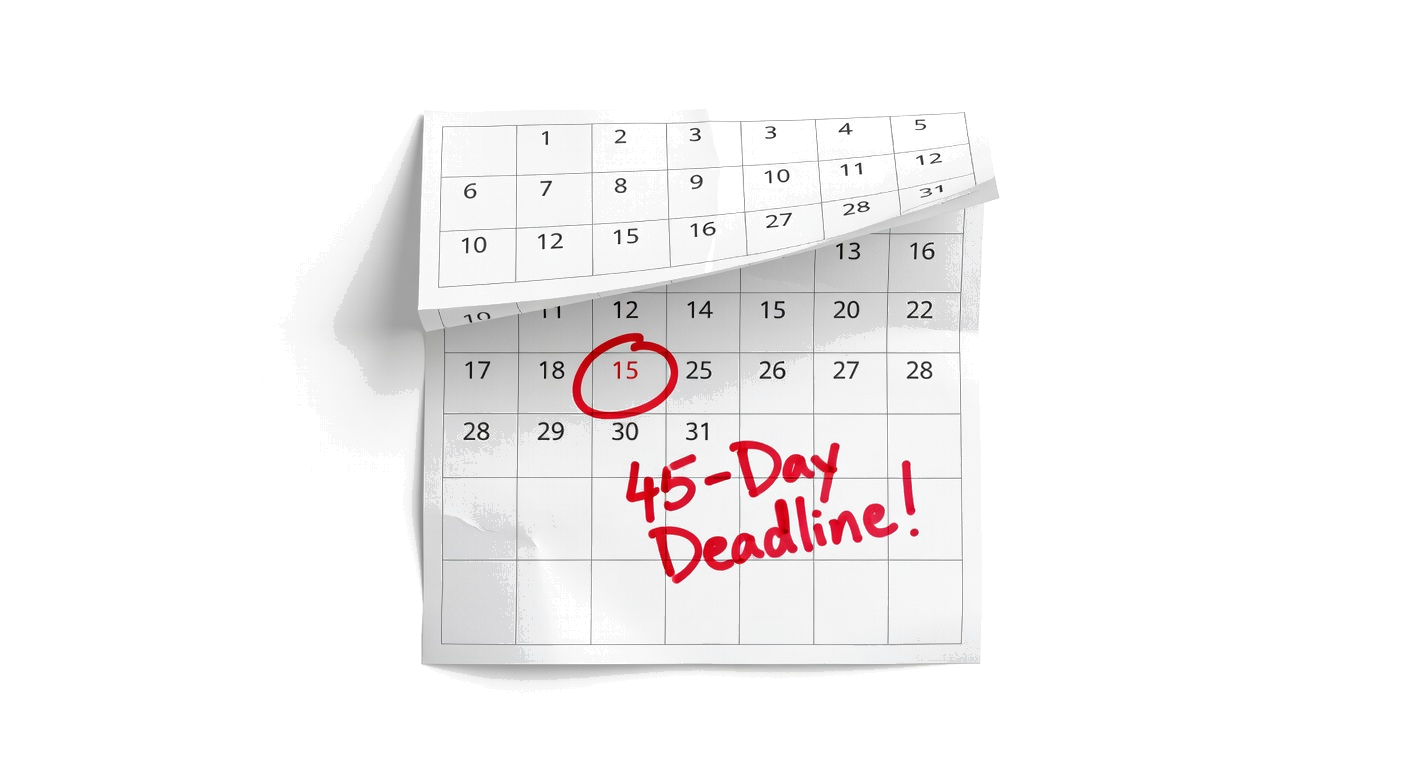

Meet Tight Deadlines

DSTs are pre-packaged and may help investors identify replacement property within the 45-day window — especially valuable when traditional property searches come up short.

Institutional-Quality Real Estate

DSTs typically hold professionally managed, institutional-grade properties — multifamily, medical office, industrial — that individual investors might not otherwise access.

Passive Ownership

No landlord responsibilities. DST investors are beneficial owners without the day-to-day management obligations of direct property ownership. No tenants, no toilets, no trash.

Portfolio Diversification

Investors may spread their exchange proceeds across multiple DSTs, potentially diversifying by property type, geography, and sponsor — reducing concentration risk.

How a 1031 Exchange Works

The mechanics, the requirements, and the critical deadlines — all in one view.

Qualify Your Property

Both the property you're selling and the one you're buying must be held for investment or business use — personal residences don't qualify. The same taxpayer (or entity) that sells must also acquire the replacement property.

Engage a Qualified Intermediary

A Qualified Intermediary (QI) must be in place before your sale closes. The QI holds all exchange funds — you cannot have actual or constructive receipt of the proceeds at any time. This is an IRS requirement, not optional.

Sell Your Investment Property

Close on the sale of your relinquished property. Proceeds go directly to your QI — the exchange clock starts now.

Identify Replacement Property

You have exactly 45 calendar days to identify potential replacement properties in writing. This deadline is strict and cannot be extended. The replacement must be of equal or greater value to defer all capital gains — any shortfall ("boot") may be taxable.

Close on Replacement Property

You must close on your replacement property within 180 calendar days of the original sale. The QI transfers funds to complete the purchase. Missing this deadline ends the exchange.

Exchange Complete — Taxes Deferred

Capital gains taxes are deferred — not eliminated — until you eventually sell without exchanging. Many investors continue exchanging indefinitely, and heirs may receive a stepped-up basis, potentially eliminating the deferred gain entirely.

Calculate Your Potential Tax Deferral

Enter your property details and see exactly how much you could save with a 1031 exchange — including a visual timeline of your critical deadlines.

1031 Exchange FAQ

Generally, any real property held for investment or business purposes qualifies. This includes rental properties, commercial buildings, raw land, and certain other real estate assets. Personal residences and property held primarily for sale (like fix-and-flip inventory) do not qualify. Since 2018, the Tax Cuts and Jobs Act limited 1031 exchanges to real property only — personal property and other asset types no longer qualify.

The 45-day identification deadline is strict and cannot be extended for any reason (except in cases of federally declared disasters in some circumstances). If you miss this deadline, the exchange fails, and you will owe capital gains taxes on the sale of the original property. This is why working with an experienced advisor early in the process is crucial.

Yes. Section 1031 is a federal tax provision and applies regardless of which state you live in. While Texas has no state income tax (which is already advantageous), you may still owe federal capital gains taxes when selling investment property. A 1031 exchange defers those federal taxes. If you own property in states with income taxes, an exchange may also defer state-level gains.

A DST is a legal entity that holds title to real property. Investors purchase beneficial interests in the trust, which qualifies as "like-kind" replacement property under IRS Revenue Ruling 2004-86. DSTs are popular in 1031 exchanges because they offer access to institutional-quality real estate with passive ownership — no landlord duties. However, DSTs are securities, involve risks, and are generally illiquid.

The amount deferred depends on your specific situation, including the property's basis, sale price, depreciation recapture, your tax bracket, and other factors. A 1031 exchange defers — not eliminates — capital gains taxes. The deferred taxes become due if you eventually sell the replacement property without doing another exchange. We recommend consulting with your tax advisor for calculations specific to your situation.

To defer all capital gains taxes, you generally need to reinvest all net proceeds and acquire replacement property of equal or greater value. Any cash you take out ("boot") may be taxable. Similarly, if you reduce your debt in the exchange, the debt reduction may also be treated as boot. Your qualified intermediary and tax advisor can help you structure the exchange properly.

Common Questions

Who qualifies as an accredited investor?

What kinds of tax-advantaged strategies do you work with?

Are alternative investments risky?

Do you coordinate with my CPA and attorney?

Do you work with investors outside of Austin?

Earl Proeger

Registered Representative of Concorde Investment Services, LLC

Grace Capital Management is a hybrid RIA that acts in a fiduciary capacity when providing investment advisory services to accredited investors in Austin and nationwide.

- Series 7General Securities Representative

- Series 63Uniform Securities Agent

- SIESecurities Industry Essentials

- NMLS #1159073Mortgage Loan Originator (TX)